July 10, 2026

Why Chasing the Wrong Numbers Can Cost You Money

Discover why impressive financial metrics can mislead investors. Learn the behavioural finance principle that helps you identify real value and avoid costly mistakes

Read more

Have you ever thought, "If only I knew how to budget, I could have saved so much more?" You're not alone. Many of us have been in situations where we've spent more than we intended, only to regret it later. But what if there was a way to take control of your finances to ensure that you're spending wisely and saving and investing for your future?

This is where budgeting comes in. It's not just about cutting costs or denying yourself pleasure. It's about understanding your income and expenses, making informed decisions, and planning for both short-term and long-term financial goals.

In this guide, we'll explore some effective budgeting hacks that can help you take control of your finances.

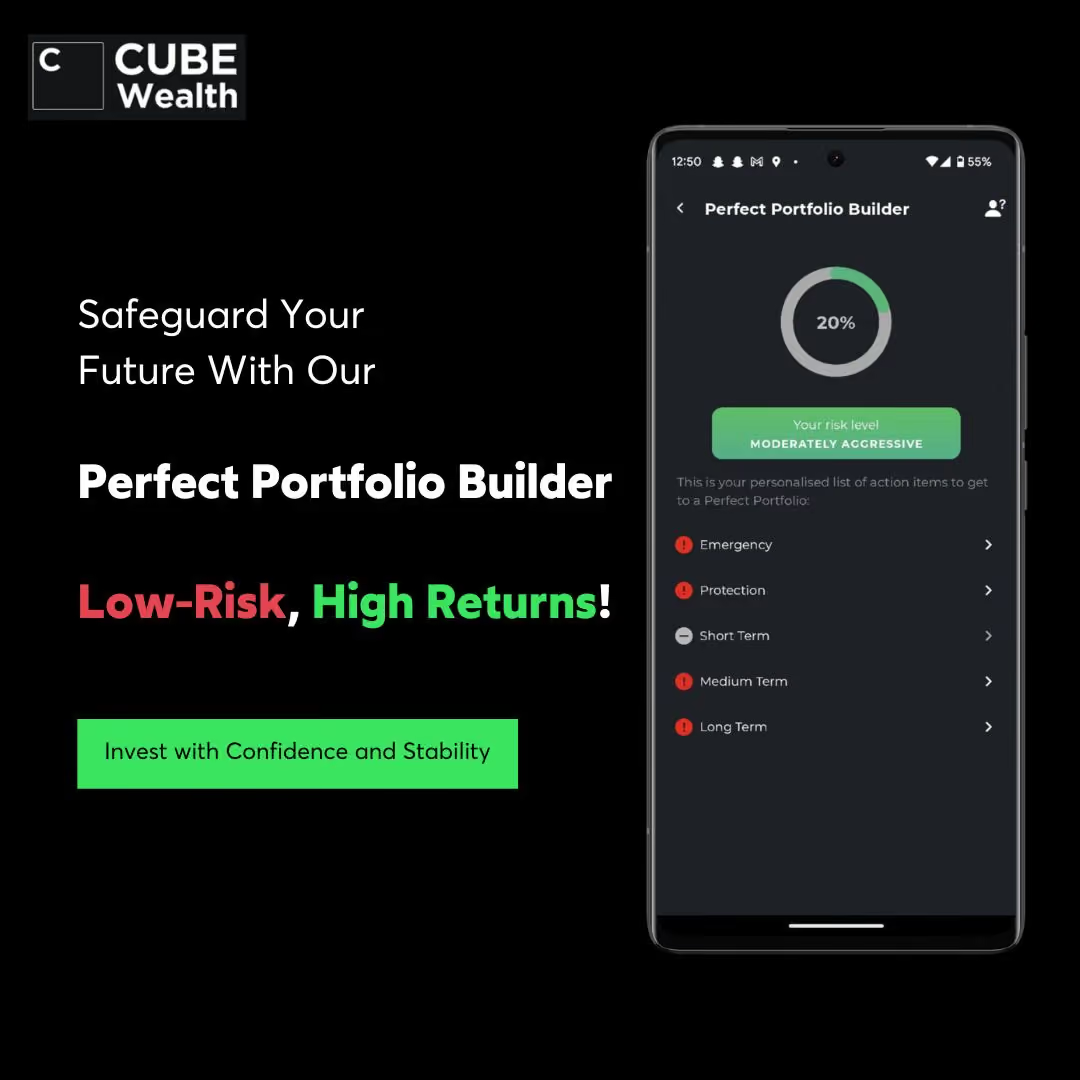

At Cube Wealth, we have a perfect portfolio builder that can assist you in creating a personalised budgeting plan for your investments. With a Cube Wealth Coach, you can confidently navigate the world of personal finance and work towards achieving your financial goals.

In the fast-paced world of busy professionals, financial management often takes a back seat amidst hectic schedules and demanding careers. However, understanding the profound impact of budgeting on one's financial stability is crucial.

Budgeting provides a panoramic view of your financial landscape, offering unparalleled clarity regarding your income, expenses, and overall financial health. By meticulously categorising and analysing your financial data, you gain a profound awareness of where your money goes and how it aligns with your goals.

Instead of feeling overwhelmed by financial uncertainties, a well-structured budget puts you in control. You decide where your money goes, making informed choices that resonate with your financial aspirations. This sense of control becomes particularly paramount when considering the ultimate goal: effective investment.

Understanding your current financial situation is the first step towards effective budgeting and financial planning. It involves assessing your income and expenses and analysing your spending patterns.

Here's how you can do it:

Start by listing all your sources of income. This could include your salary, any side jobs, rental income, dividends, etc. Be sure to consider all possible sources of income, no matter how small they might seem. This will give you a clear picture of your total income.

Next, track all your monthly expenses. This includes fixed expenses like rent or mortgage, utilities, groceries, transportation, health care, and debt payments, as well as variable expenses like dining out, entertainment, and shopping. You can use a budgeting app or a simple spreadsheet to track your expenses.

Once you have a clear picture of your income and expenses, you can start analysing your spending patterns. Start by identifying your discretionary and non-discretionary expenses. Non-discretionary expenses are those that are necessary for survival, such as food, shelter, and healthcare. Discretionary expenses, on the other hand, are non-essential expenses that enhance your lifestyle, such as dining out, entertainment, and vacations.

After identifying your discretionary and non-discretionary expenses, look for areas where you can potentially save money. This could be cutting back on dining out, cancelling unused subscriptions, or switching to a cheaper phone plan. Remember, every little bit counts when it comes to saving money.

Setting financial goals is a crucial part of financial planning. It gives you a clear direction and helps you stay focused on your financial journey.

Here's how you can set and prioritise your financial goals:

An emergency fund is a stash of money set aside to cover the financial surprises life throws your way. These unexpected events can be stressful and costly. Here are some examples: losing your job, an illness, or a major house-related expense like a leaky roof. Aim to save three to six months' worth of living expenses in your emergency fund.

Debt can be a significant burden and can prevent you from achieving your financial goals. Make a list of all your debts: credit cards, student loans, car loans, personal loans, payday loans, etc. Prioritise them based on the interest rate and the outstanding balance. Start with the debt that has the highest interest rate.

Retirement may seem far off in the future, but it's important to start saving for it now. The earlier you start, the more time your money has to grow. Consider contributing to retirement accounts like a 401(k) or an IRA. Aim to save at least 15% of your income for retirement.

Investing is a great way to grow your wealth over time. Set clear investment goals, such as buying a house, starting a business, or funding your child's education. Consider your risk tolerance and time horizon when choosing your investments.

Once you've set your financial goals, it's important to prioritise them based on their urgency and importance. Here's how you can do it:

Creating a realistic budget is the first step towards taking control of your finances. It involves understanding your income and expenses and allocating your income to various expense categories. Here's how you can do it:

The first step in creating a budget is to understand your income and expenses. Start by listing all your sources of income. This could include your salary, any side jobs, rental income, dividends, etc. Next, list all your expenses. This could include rent or mortgage, utilities, groceries, transportation, health care, debt payments, and so on.

Once you have a clear picture of your income and expenses, you can start allocating your income to these expense categories. The goal is to ensure that your income covers all your expenses, with some leftover for savings and investments.

The 50/30/20 rule is a simple yet effective budgeting technique. It involves dividing your after-tax income into three categories: necessities, discretionary spending, and savings and investments.

Allocate 50% of your income to necessities. These are the things you absolutely need to live and work. This includes rent or mortgage, utilities, groceries, health care, and transportation. If you're spending more than 50% of your income on necessities, you might need to look for ways to cut back.

Allocate 30% of your income to discretionary spending. These are non-essential items that enhance your lifestyle. This includes dining out, entertainment, hobbies, vacations, and so on. This is the category where you have the most flexibility. If you need to cut back, start here.

Allocate 20% of your income to savings and investments. This includes emergency savings, retirement accounts, and other investments. If you're not saving at least 20% of your income, you might need to cut back on your necessities or discretionary spending.

Remember, the key to a successful budget is to make it realistic. It should reflect your lifestyle and financial goals. If you're just starting out, it might take some time to get your budget right. But with patience and perseverance, you can create a budget that works for you.

Taking control of your finances might seem daunting, especially if you're a busy professional. But with the right strategies and tools, it can become a seamless part of your routine. Remember, the key to successful budgeting and investing is understanding your income and expenses, making informed decisions, and planning for both short-term and long-term financial goals.

So, are you ready to take control of your finances? Start budgeting and investing today! Your journey towards financial freedom starts here. At Cube Wealth, we offer curated investment options and personalised financial advice just for you. With our Perfect Portfolio Builder, you can easily create a diversified investment portfolio tailored to your financial goals and risk tolerance. Our team of expert advisors will guide you every step of the way, ensuring that your investments align with your unique needs. Plus, our user-friendly app makes it convenient to track your progress and make adjustments as needed. Don't wait any longer—start taking control of your finances and building wealth with Cube Wealth today!

Budgeting is the process of creating a plan for your income and expenses. To create a budget, follow these steps:

1. Identify Income: List all income sources.

2. Track Expenses: Record all monthly expenses.

3. Categorise Expenses: Group expenses into categories.

4. Set Goals: Define short-term and long-term financial goals.

5. Create a Budget: Allocate money to each expense category based on income, expenses, and goals.

6. Implement Budget: Follow the budget, sticking to the allocated amounts.

7. Review and Adjust: Regularly review and adjust the budget as needed.

If you find yourself consistently going over your budget, it may be helpful to identify areas where you can cut back on expenses or find ways to increase your income. Additionally, consider seeking advice from a financial advisor or exploring resources that offer tips and strategies for managing your finances more effectively.

The amount you should save each month depends on your individual financial goals and circumstances. However, a general guideline is to aim for saving at least 20% of your income. This can help build an emergency fund, contribute to retirement savings, and work towards other long-term financial objectives. It's important to find a balance between saving and covering your necessary expenses, so consider adjusting this percentage based on your specific needs and priorities.

The 50/30/20 rule in budgeting is a popular guideline that suggests allocating 50% of your income towards necessary expenses such as rent, utilities, and groceries, 30% towards discretionary spending like entertainment and dining out, and 20% towards savings and debt repayment. This rule can serve as a helpful starting point for budgeting, but it's important to customise it based on your own financial situation and priorities. Remember to regularly review and adjust your budget as needed to ensure it.

Budgeting with an irregular income can be challenging, but there are strategies you can use to manage it effectively. One approach is to create a budget based on your average monthly income over a longer period of time, such as six months or a year. This can help smooth out the fluctuations in your income and give you a more realistic picture of what you have to work with. Additionally, it's important to build an emergency fund to cover any unexpected expenses or income gaps. This can provide a safety net and help alleviate financial stress during periods of lower income.

Another strategy is to prioritise your expenses and focus on essential needs first, such as housing, utilities, and food. By identifying your non-negotiable expenses, you can allocate your limited resources accordingly and make sure your basic needs are met.

Schedule a call based on your convenience. And get an expert to help you invest.

.png)

The financial life game that makes learning fun!

Let's get in touch

Want the best

investment blog delivered straight to your inbox?

Grow your money without wasting time

on stock picking, poring over excel sheets, financial news, analyzing market trends, tracking the Sensex, researching company fundamentals, comparing mutual funds, reading financial reports, trying to predict the future & losing your sanity!