July 10, 2026

Why Chasing the Wrong Numbers Can Cost You Money

Discover why impressive financial metrics can mislead investors. Learn the behavioural finance principle that helps you identify real value and avoid costly mistakes

Read more

For decades, fixed-income investing in India followed a simple pattern: safety first, returns later. Fixed deposits, traditional bonds, and conservative debt products were the default choices for investors who wanted stability. But as wealth grows and inflation rises, this approach stops working. Low returns slowly erode purchasing power, while higher-yield products introduce risks that most investors don’t fully understand.

This is where Securitized Debt Investments (SDI) are changing the landscape of fixed-income investing.

SDI creates a structured way to generate predictable income while maintaining capital protection. It combines asset-backed security, diversification, and regulatory oversight into a single investment structure. For investors building long-term wealth, SDI is no longer just an alternative fixed-income option — it is becoming a core stability layer in modern portfolios.

Securitized Debt Investments are structured fixed-income instruments created by pooling together multiple loans or bonds — such as business loans, consumer loans, or asset-backed financing — and converting them into investable securities. The cash flows generated from borrower repayments are passed on to investors as regular income.

Instead of lending to a single borrower or institution, investors gain exposure to a diversified pool of underlying assets. This diversification reduces concentration risk and creates more stable income streams.

In simple terms, SDI allows investors to earn predictable returns from real economic activity — businesses repaying loans, consumers servicing credit, and assets generating cash flows — rather than relying only on issuer promises.

SDI operates under SEBI and RBI regulatory frameworks, ensuring defined rules for structuring, disclosures, governance, and investor protection.

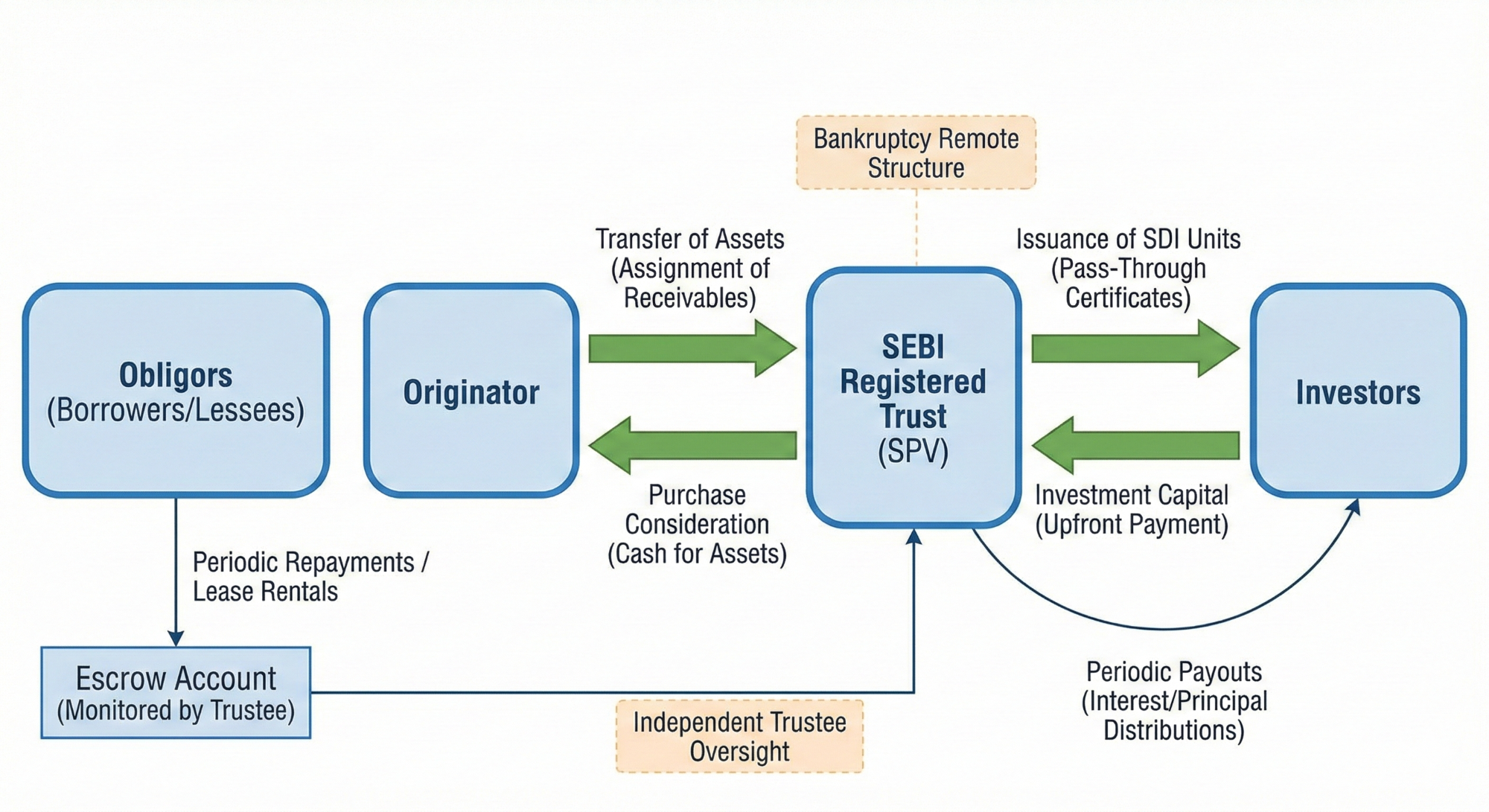

Securitized Debt Investments are built on a regulated securitisation structure designed to protect investor capital and ensure clean, predictable cash flows.

At the core of the structure is the Originator, who facilitates the investment opportunity by creating a securitisation framework using a pool of underlying debt instruments. This typically involves the securitisation of a pool of bonds or loan assets issued by established lending institutions such as NBFCs.

The Originator assigns the future receivables from these underlying bonds or loans — including both principal and interest payments — to a special purpose trust (Trust). This Trust is set up and managed by an independent SEBI-registered trustee, ensuring regulatory oversight and structural independence.

The Trust uses the money received from investors to purchase these receivables. In return, investors receive monthly or quarterly interest payouts along with staggered principal repayments, which originate directly from the underlying loan or bond cash flows.

A critical feature of this structure is bankruptcy remoteness. This means that even if the Originator or any intermediary entity faces financial distress, the receivables and cash flows from the underlying assets remain protected and continue to flow to investors through the Trust.

From a tax perspective, returns are distributed by the Trust on a pre-tax basis (subject to withholding tax where applicable), and taxation generally applies only to the interest income component earned from the underlying securities.

In simple terms, SDI creates a ring-fenced, regulated structure where:

This structure is what makes SDI fundamentally different from traditional debt products — it is asset-backed, ring-fenced, regulated, and structurally protected, not just yield-driven.

Most fixed-income investors face a trade-off between safety and returns. Fixed deposits provide security but low income. Bonds offer higher yields but introduce credit risk. Debt funds fluctuate with market movements. High-yield products often hide structural risk.

Investors want stable income, capital protection, predictable cash flows, and portfolio stability. SDI fills this gap by combining structured protection with income generation.

Smart SDI investing is not about chasing yield. It is about understanding structure and risk protection.

Key evaluation pillars include:

SDI structures are credit-rated based on asset quality, borrower strength, and pool performance. Only investment-grade structures provide strong downside protection.

Security cover includes over-collateralisation, cash collateral, and excess interest buffers. This ensures that investor capital remains protected even if some borrowers default.

Strong SDI structures are stress-tested to withstand payment delays and partial defaults without impacting investor returns.

Tenure impacts predictability and risk. Medium-duration structures balance income stability with uncertainty management.

Diversification across geographies, borrowers, and sectors reduces systemic risk and concentration exposure.

The quality, governance, and financial stability of the lending institution directly impact long-term performance and reliability.

SDI is ideal for investors seeking stable income, lower volatility than equity, predictable cash flows, and long-term capital preservation. It suits income-focused portfolios, conservative wealth strategies, retirement planning structures, and NRIs seeking structured fixed-income exposure to India.

SDI works best as a fixed-income layer within a diversified portfolio — not as a speculative return product.

The real power of SDI lies in how it is used. It should not replace growth assets. It should balance them.

SDI complements equity, PMS strategies, mutual funds, passive investments, bonds, and global assets by providing stability, income, and resilience.

Effective SDI integration includes structured allocation sizing, diversification across multiple SDI deals, tenure staggering for liquidity management, income planning, and ongoing portfolio monitoring. This transforms SDI into a long-term income engine rather than a short-term yield play.

Securitized debt is not about high returns.

It is not about yield chasing.

It is not about speculation.

It is about income stability, capital protection, and financial resilience.

Smart investors don’t ask:

Which SDI gives the highest return?

They ask:

How does SDI protect and stabilize my wealth?

That question changes everything.

A securitized debt investment is a fixed-income instrument created by pooling multiple loans or bonds and converting them into investable securities. Investors earn regular income from repayments, with structured protection, asset backing, and predictable cash flows.

SDI works by transferring loan or bond receivables into a regulated trust structure, where investor funds are used to purchase receivables and repayments are distributed as income.

Safety depends on structure, security cover, credit quality, diversification, and regulatory compliance. Well-structured SDIs use multiple layers of protection.

SDI is suitable for investors seeking stable income, capital protection, and low-volatility fixed-income exposure.

SDI and bonds serve different purposes. SDI offers asset backing and structured protection, while bonds rely primarily on issuer credit quality.

Yes, SDI structures operate under regulatory frameworks governed by SEBI and RBI.

It is a fixed-income investment created by pooling multiple loans or bonds and converting them into securities that generate regular income.

Returns come from the interest and principal repayments of the underlying loan or bond pool.

Risk depends on structure, credit rating, security cover, diversification, and originator quality. Strong SDI structures manage downside risk effectively.

Yes, securitized debt investments operate under SEBI and RBI regulatory frameworks.

No, NRIs cannot invest in securitized debt investments for structured fixed-income exposure to India.

SDI should act as a fixed-income stability layer alongside equity and growth investments.

Schedule a call based on your convenience. And get an expert to help you invest.

.png)

The financial life game that makes learning fun!

Let's get in touch

Want the best

investment blog delivered straight to your inbox?

Grow your money without wasting time

on stock picking, poring over excel sheets, financial news, analyzing market trends, tracking the Sensex, researching company fundamentals, comparing mutual funds, reading financial reports, trying to predict the future & losing your sanity!